What is Step Variable Cost?

A Step Variable Cost is an expense that remains constant within a given range but can increase or decrease when outside that range.

“Costs that are constant over a range of production.” -Iowa State University

Understanding Step Variable Cost

Step variable cost, also known as step costs, are affected by changes in supply and demand. Step costs are commonly fixed expenses paid from an organization’s floating capital. These fixed expenses can become variable expenses when:

- Demand increases

- Demand decreases

- Bottlenecks occur

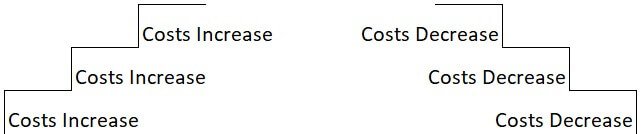

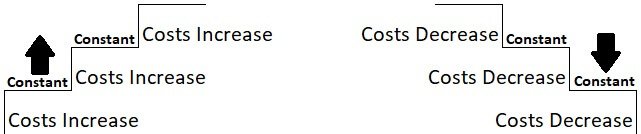

As supply and demand changes, a flight of stairs is a good visual representation of step variable cost. The upward or downward movement depicts changes in cost.

Businesses generally anticipate a certain amount of fixed or budgeted cost when activity levels remain constant over an expected range. If activity levels spike upward or downward unexpectedly, costs can increase or decrease disproportionately.

From a production cycle standpoint, costs per unit tend to decrease as the number of units produced increase until the occurrence of a step variable cost. In such a situation, production capacity limits may have been exceeded.

Example One

The salary of a shop floor supervisor in a production department overseeing 1,500-2,000 units produced daily is an example of this concept.

A second shop floor supervisor, along with additional support personnel, would be necessary if demand for the product increased to 2,001-4,000 units per day. Therefore, the total salary costs of shop floor supervisors vary with changes in product demand.

One shop floor supervisor has daily capacity limits above 2,000 units whereby two shop floor supervisors have daily capacity limits up to 4,000 units.

Example Two

A bakery shop can serve up to 20 customers per hour with one cashier. Sometimes the shop has 20 customers per hour and other times it has 0 customers in an hour. The owner pays the cashier the same amount each week regardless of the number of customers per hour.

Due to the recent closure of a local competitor the bakery shop has been receiving up to 30 customers per hour. The shop’s one cashier has been struggling at times to assist all customers during the busiest hours, resulting in lost business.

The owner eventually decides to hire a second cashier due to the shop’s additional customer flow. Although business hasn’t doubled, the bakery shop now has two cashiers.

Additional Resources

Other helpful articles may include:

What is Cost of Nonconformance?

Stockout Cost: Understanding

What is Cost Based Pricing?